Introduction: Why Everyone Is Talking About RBI Repo Rate in 2026

Have you noticed how news channels keep talking about the RBI Repo Rate 2026?

And you might be thinking…

“Okay, but how does this affect me?”

Don’t worry. In this article, I’ll explain everything in simple, beginner-friendly language — like a normal conversation.

By the end of this post, you’ll clearly understand:

-

What RBI Repo Rate is

-

Why it changes

-

How it affects your EMI

-

How it impacts savings and inflation

-

What to expect in 2026

Let’s start from the basics.

What is RBI Repo Rate?

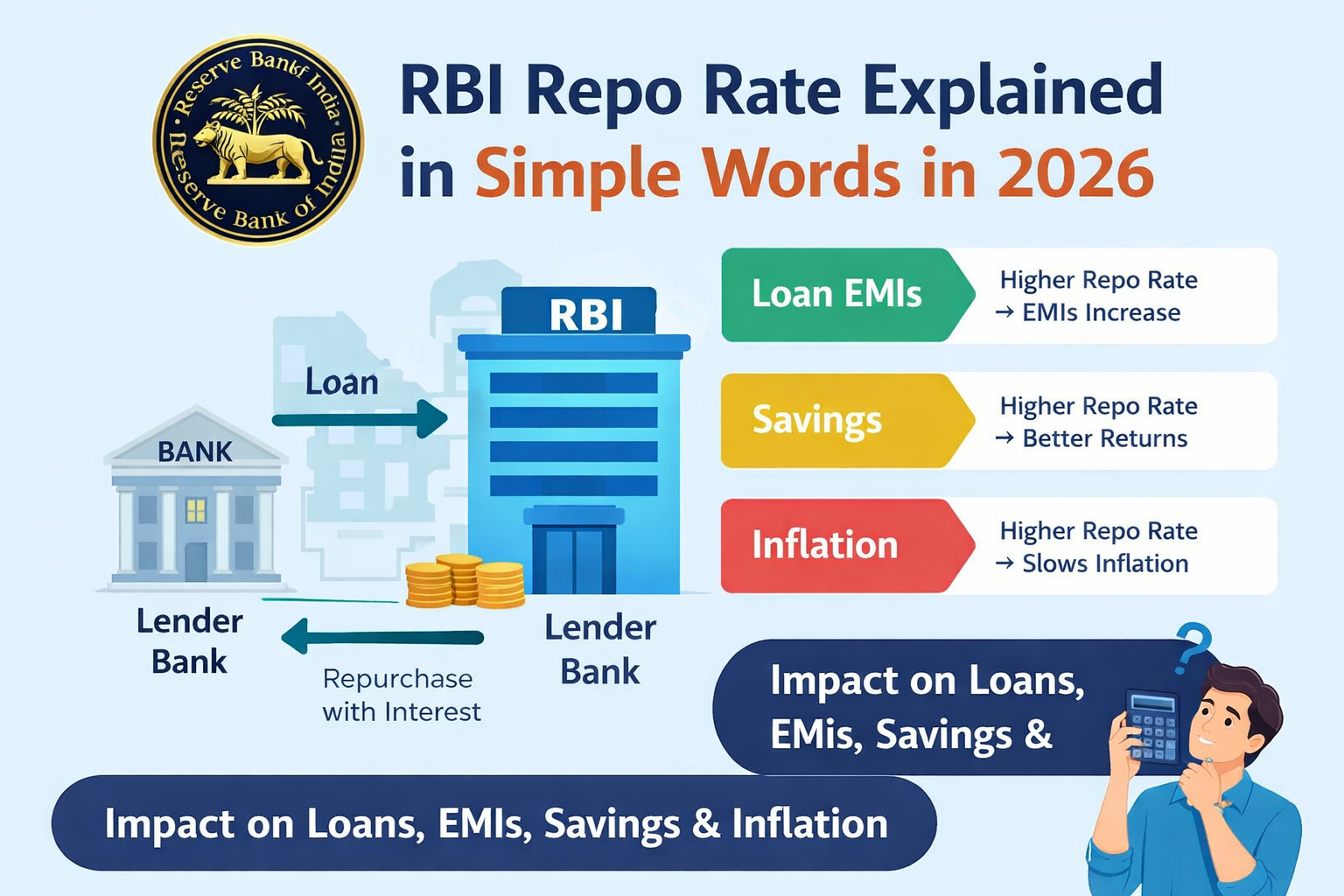

The RBI Repo Rate is the interest rate at which the Reserve Bank of India lends money to commercial banks.

Let’s simplify that.

Sometimes banks need extra money. When they don’t have enough cash, they borrow from RBI. The interest they pay on that borrowed money is called the Repo Rate.

The word “Repo” means Repurchase Agreement. Banks sell government securities to RBI and promise to buy them back later at a slightly higher price. That extra amount is the interest.

In one simple line:

👉 Repo rate is the rate at which RBI gives loans to banks.

Why Does RBI Change the Repo Rate?

Now the big question.

Why does RBI increase or decrease the repo rate?

The main reason is to control:

-

Inflation (rising prices)

-

Economic growth

-

Money supply in the country

Think of repo rate like a volume control button for the economy.

If prices are rising too fast → RBI increases repo rate.

If the economy is slowing down → RBI reduces repo rate.

Simple.

How RBI Repo Rate 2026 Works in Real Life

Let’s understand with practical situations.

When RBI Increases Repo Rate

-

Banks borrow money at higher interest

-

Loan interest rates increase

-

Home loan EMI goes up

-

Personal loans become expensive

-

People borrow less

-

Spending reduces

-

Inflation slows down

So if repo rate increases in 2026, loans may become costly.

When RBI Decreases Repo Rate

-

Banks get money at lower interest

-

Loan rates reduce

-

EMIs become cheaper

-

People borrow more

-

Spending increases

-

Economy grows faster

So if repo rate decreases in 2026, loans may become cheaper.

See how directly it affects your pocket?

How RBI Repo Rate 2026 Affects You Personally

Now let’s make this more personal.

1️⃣ Impact on Home Loan EMI

If you have a floating rate home loan:

-

Repo rate increases → EMI increases

-

Repo rate decreases → EMI decreases

Even a 0.25% change can affect your total interest by lakhs over time.

2️⃣ Impact on Car Loans & Personal Loans

Planning to buy a car in 2026?

If repo rate is high → Loan will be expensive.

If repo rate is low → Loan will be cheaper.

So timing matters a lot.

3️⃣ Impact on Fixed Deposits and Savings

Here’s something interesting.

When repo rate increases:

-

FD interest rates may increase

-

You may earn better returns

When repo rate decreases:

-

FD returns may reduce

So borrowers prefer low repo rate.

Savers prefer high repo rate.

4️⃣ Impact on Inflation

Inflation means rising prices of daily items like vegetables, petrol, groceries.

If inflation becomes too high, RBI increases repo rate to reduce spending.

Higher interest → Less borrowing → Less spending → Lower inflation.

That’s the logic behind it.

RBI Repo Rate 2026: What Can We Expect?

In 2026, repo rate decisions will depend on:

-

Inflation trends

-

Economic growth rate

-

Global economic conditions

-

Government fiscal policies

If inflation stays high, RBI may keep repo rate higher.

If economic growth slows down, RBI may reduce it to support businesses and consumers.

Repo rate is not fixed forever. It keeps changing based on economic conditions.

Difference Between Repo Rate and Reverse Repo Rate

Many beginners get confused here. Let’s clear it simply.

-

Repo Rate → RBI lends money to banks

-

Reverse Repo Rate → Banks lend money to RBI

Repo rate controls borrowing.

Reverse repo controls liquidity in the banking system.

Now you won’t confuse them again 😊

Why RBI Repo Rate 2026 Is Important for Beginners

You might think this topic is only for economists.

But actually, it matters if you are:

-

A salaried employee

-

A business owner

-

A student planning an education loan

-

A first-time home buyer

-

An investor

Even if you don’t take loans, repo rate affects:

-

Job market

-

Business growth

-

Stock market

-

Investment returns

Understanding RBI Repo Rate 2026 makes you financially smarter.

Smart Financial Tips for 2026

Here are some simple tips you can follow:

✔ Avoid unnecessary loans if repo rate is rising

✔ Consider refinancing if repo rate falls

✔ Lock FDs when interest rates are high

✔ Compare loan offers before borrowing

✔ Track RBI policy meetings

Small awareness can save big money.

How to Stay Updated About RBI Repo Rate

RBI reviews interest rates during monetary policy meetings (usually every two months).

You can stay updated by:

-

Watching financial news

-

Checking RBI announcements

-

Reading finance blogs

-

Talking to your bank manager

If you are new to managing money, you should also read:

👉 Internal Link: https://yourwebsite.com/budgeting-basics-for-beginners

It will help you understand money management from scratch.

Final Conclusion: RBI Repo Rate 2026 in Simple Words

Let’s quickly recap.

👉 RBI Repo Rate is the interest rate at which RBI lends money to banks.

👉 It affects your home loan EMI.

👉 It impacts savings and FD returns.

👉 It helps control inflation.

👉 It influences the entire economy.

You don’t need a finance degree to understand this.

Just remember:

When repo rate changes, your money is affected somewhere.

Now you can confidently explain RBI Repo Rate 2026 to anyone — even in a simple conversation.

Stay informed. Stay financially smart. 🚀

Understanding RBI Repo Rate 2026 helps you make smarter financial decisions in changing economic conditions.

If you are new to money management, read our complete guide on Budgeting Basics for Beginners to understand how to manage your monthly income smartly.

What Is RBI and What Does It Do? (Beginner Guide) in 2026

You can check the latest repo rate updates directly on the official website of the Reserve Bank of India.

Link:

https://www.rbi.org.in